No products in the cart.

The widebody freighter fleet part III: New widebody operators gravitate toward 767Fs

Today we offer the final section of the 2019 edition of our annual widebody freighter fleet analysis. We began this year’s analysis of the worldwide widebody freighter fleet earlier this week with a look at the composition of the fleet on a carrier-by-carrier basis. You can review part I here. Part II continued with an analysis of fleet changes on a type-by-type basis. Today we conclude with a review of operators that began or ceased widebody freighter operations in 2018, and look ahead to the future trajectory of the widebody freighter fleet.

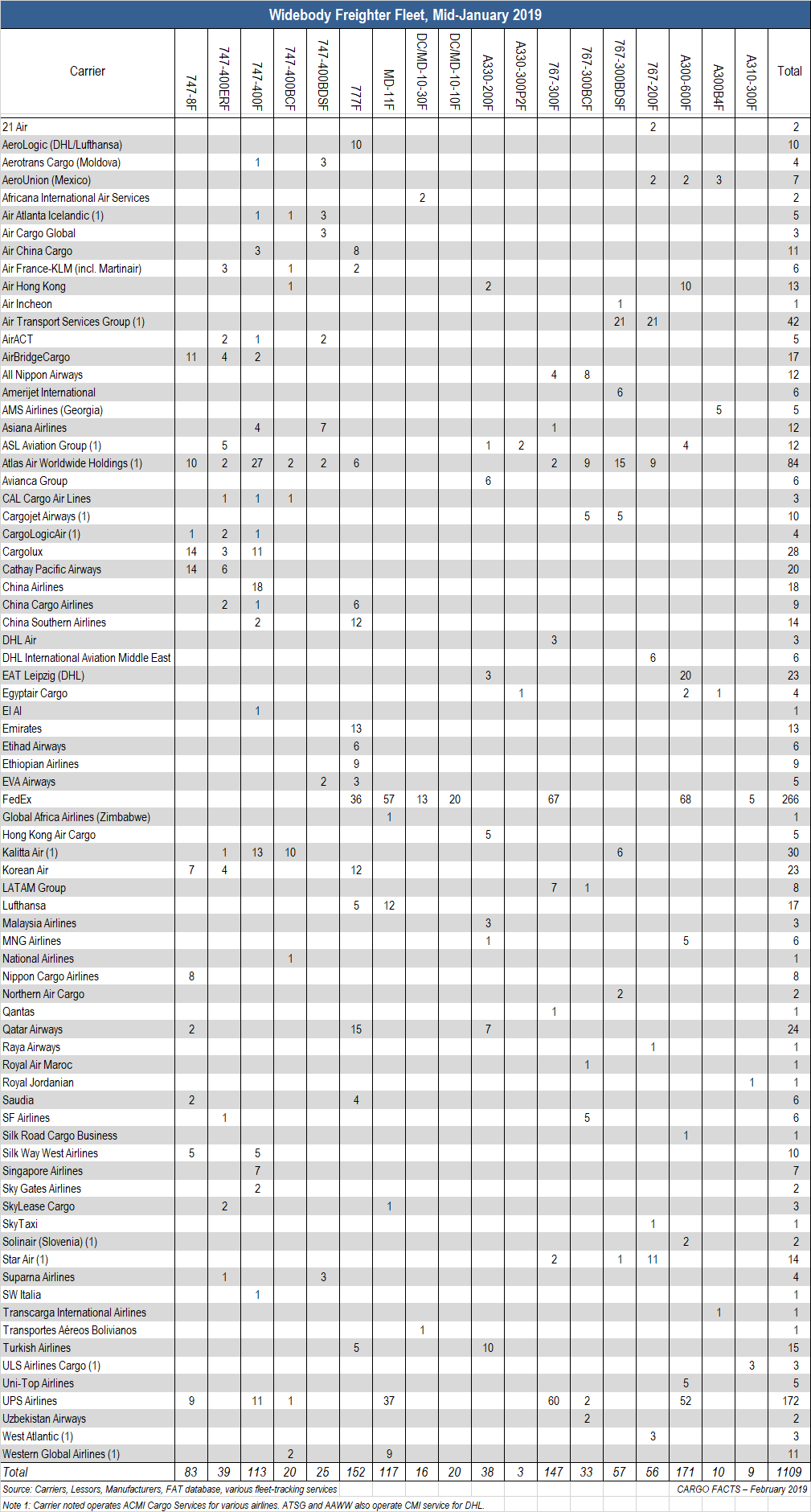

The chart below shows that the 1,109 widebody freighters in active service are operated by a total of seventy-six carriers. This is up from seventy-three carriers last year, but still a decline from eighty-five just three years earlier, as four new carriers have entered the market, while one has exited:

Gone from last year are:

- KF Cargo: This Canada-based carrier sold its DC/MD-10-30Fs and has ceased widebody freighter operations.

New to the list this year are:

- Air Incheon: Korea-based Air Incheon added a 767-300BDSF in 2018, and could add a second in 2019.

- Africana International Air Services: a Uganda-based startup that is in the process of adding a pair of ex-KF Cargo DC/MD-10- 30Fs to its fleet.

- Royal Air Maroc: Morocco-based Royal Air Maroc introduced a 767-300BCF to its fleet in 2018.

- SkyTaxi: This Poland-based airline added a 767-200F to its fleet in 2018, and has options for a second, exercisable in 2019.

Although there remain thirty-seven 747-400Fs (mostly conversions) and fifty MD-11Fs in storage, Cargo Facts believes that most aircraft worthy of returning to service, are already there, and that the remaining units in storage will never fly again.

Regarding the order backlog, twelve carriers, one lessor, and one unidentified customer have 146 widebody production freighters on order with Airbus and Boeing. Of these orders, 48% – sixteen 777Fs and fifty-four 767-300Fs – are for FedEx. The remainder are spread among the other nine carriers, lessor Hong Kong International Aviation, and one unidentified customer. There remain only three outstanding orders for the A330-200F, and all three are for Turkey-based MNG Airlines, which took delivery of its first of four ordered in 2013 and has not taken another since.

There has been an upsurge in orders for medium widebody P-to-F conversions over the last four years, driven primarily by the launch and expansion of Amazon’s dedicated air freight operation, but also by strong demand from integrators. There are currently active programs for P-to-F conversion of 747-400s (Bedek), A330-200s/-300s (EFW), 767-300s (Bedek and Boeing), and A300-600s (EFW and Turkish Technic). Of these, the 747 program is effectively dead, and once EFW completes the last remaining A300- 600 conversions currently in its backlog, that program will also end.

But continuing robust demand for 767-300 conversions means that for the foreseeable future, Bedek and Boeing will have their hands full. When suitable conversion feedstock for 767 conversions does eventually wane, A330-300 conversions should take up most of the slack.

Regarding the A330, Airbus launched conversion programs for both the -200 and -300 variants, through a joint venture with EFW and ST Aerospace six years ago. EFW has taken orders for A330-200 and -300 P-to-F conversions from Egyptair and DHL, and has at least eight additional units on firm order.

Although the precise size of the order backlog is unclear at this point, there have been a number of developments, which are indicative of a healthy backlog of forty to fifty units.

In December, ATSG’s leasing affiliate, Cargo Aircraft Management (CAM), secured rights to twenty 767-300ERs slated to come out of passenger service with American Airlines over the next three years. A few days later, CAM, announced it had agreed to lease ten additional freighter-converted 767-300Fs to Amazon, with five delivered per year in 2019 and 2020. Amazon’s deal with ATSG also includes warrant incentives for up to seventeen additional freighters from ATSG.

Prior to announcing the deal with Amazon, ATSG estimated it would place between eight and ten 767-300Fs in service during 2019. Besides ATSG, a number of other carriers have conversion orders in place with Bedek Aviation Group and Boeing, including SF Airlines, Kalitta Air, and CargoJet.

Overall, the total freighter backlog for both production and conversion models is likely between 190 and 200 units, up slightly from last year’s 150 production freighters and thirty-five conversions. Although the rate at which the air cargo market is expanding slowed in the second half of 2018, healthy backlogs for both freighter-converted and production 767-300Fs, and the 777F, will contribute to growth of the widebody freighter fleet in 2019.

Those interested in learning more about the future trajectory of the widebody freighter fleet are invited to join us at Cargo Facts Asia 2019, to be held 15-17 at the Langham Shanghai where Cargo Facts Consulting will present the 2019 edition of its annual twenty-year Freighter Forecast. For more information, or to register, visit www.cargofactsasia.com.

{kind=link}