No products in the cart.

The widebody freighter fleet part I: growth returns!

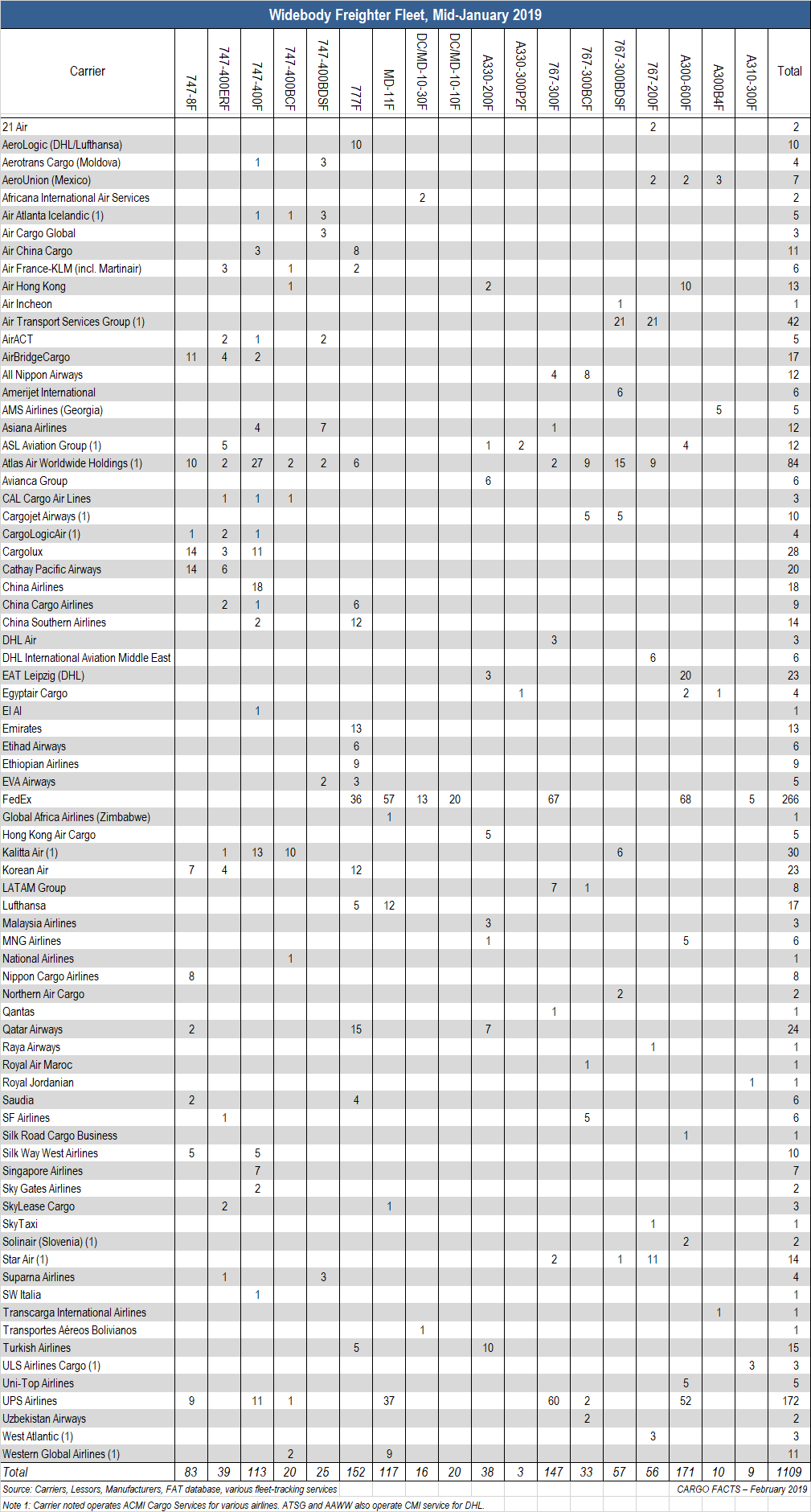

Today we begin a multi-part analysis of the worldwide fleet of widebody jet freighters in commercial service as of 15 January 2019. We start with a look at the entire fleet – which carriers are operating which freighters – and in the coming days will move on to the ways in which the fleet has changed on a type-by-type and operator-by-operator basis. Needless to say, by the time you read this there will have been changes – freighters parked or reactivated, as well as new deliveries and new orders (such as AeroLogic’s 777F delivery, which is expected in the early part of this year) – but to make year-on-year comparisons meaningful, we use 15 January as our cutoff date.

After a post-2008 recession slump, air freight demand grew steadily, during the five-year period from 2012 through 2016, increasing at an average annual growth rate of 3.5%. Despite this modest growth in demand, the number of widebody freighters in service declined 1.0% over the five-year period, as carriers and lessors parked older freighters at a faster rate than they took delivery of new ones.

2017 was different, at least on the demand side. The growth in air freight demand that began in late 2016 accelerated to the point that worldwide air cargo traffic in 2017 was up close to 10% over 2016. Expansion of the freighter fleet, however, did not increase in parallel, and the global widebody fleet expanded by just 3.2% over the previous year.

As we look at the fleet in mid-January 2019, we count 1,109 widebody jet freighters in commercial service worldwide with seventy-six carriers and carrier groups (see chart below) an increase of 74 widebody freighters, up 7.1% over the total a year ago – an indicator that capacity has been added to accommodate recent demand growth.

See also: Production freighter orders in 2018 part I: the year of the 777F

Note: Not shown in the chart are carriers that lease widebody freighters on an ACMI basis, but do not operate any on their own behalf. This includes carriers such as Astral Aviation, which ACMI-leases a 747-400F from Air Atlanta Icelandic. For carriers that both operate their own freighters and also ACMI-lease additional lift, we show only the carrier’s own freighters. Regarding aircraft operated on a CMI basis (Crew, Maintenance and Insurance), we show these in the fleet of the carrier that flies them.

The global widebody fleet is now 9.7% larger than it was at the previous high point, recorded at the end of 2011, when the fleet count stood at 1,012 units. After reaching a peak of 1,012 units in 2011, the fleet shrank as deliveries slowed and carriers parked older freighters, and it is only now, seven years on, that growth has returned. The number of widebody freighters in service is well above past highs.

Over the past year, airfreight capacity has also been added at a significant clip, but by how much? Available airfreight capacity changes with each adjustment to the freighter fleet, and given the payload variance between different freighter types, an expanding freighter fleet does not necessarily lead to a parallel increase in theoretical capacity. For example, if a carrier replaces a 118-tonne capacity 747-400F with a larger, 140-tonne capacity 747-8F, that results in a net capacity increase. Sometimes, however, the reverse happens, as was the case when Taiwan-based EVA Air began replacing its 747-400Fs with slightly smaller 777Fs.

Regardless, between January 2018 and 2019, the total widebody freighter payload increased by 7.7% as carriers took delivery of widebody freighters, and as units that were previously parked were returned to service. In a change from recent years, maindeck freighter capacity grew rapidly even as cargo-friendly A330s, 787s, A350s, and 777s are delivered to combination carriers worldwide to meet growing passenger demand.

Although the order backlog for A330, A350, A380, 787, 777, and 777X passenger aircraft remains robust, and belly space in passenger aircraft continues to be utilized to a high degree, there is a consensus that belly cargo won’t overtake maindeck capacity in the near-term. Despite being a cheaper option compared to widebody freighters, much of the capacity exists on routes that do not overlap with air cargo transportation demands or with inadequate capacity. Additionally, a number of goods cannot travel by air, and there is still a preference for containerized or palletized freight, which the majority of the world’s passenger fleet cannot accommodate. Still, there is concern that the pendulum could shift during the next downturn.

Part II will examine the fastest-growing freighter fleets by carrier and analyze how global freighter fleets have changed on a type-by-type basis.

Those interested in learning more about widebody freighters and the forecasted growth of the global freighter fleet in the coming years are invited to join us at Cargo Facts Asia 2019, to be held 15-17 at the Langham Shanghai. For more information, or to register, visit www.cargofactsasia.com.

{kind=link}