No products in the cart.

Freighter distribution within the widebody fleet: Part II

Yesterday, we began a two-part look at the way the 1,109 widebody freighters currently in operation are distributed within the fleet by type (see part I). Today, we continue the analysis by turning the focus to distribution by manufacturer, operator type, and by geographical region.

Yesterday, we began a two-part look at the way the 1,109 widebody freighters currently in operation are distributed within the fleet by type (see part I). Today, we continue the analysis by turning the focus to distribution by manufacturer, operator type, and by geographical region.

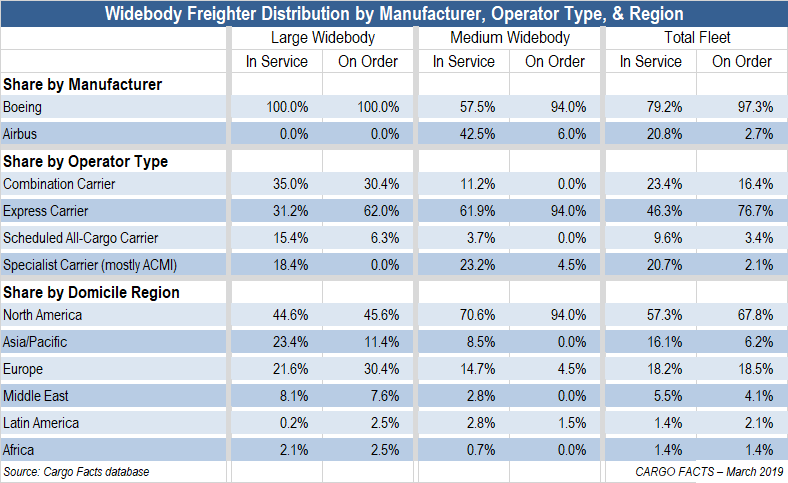

The table at right shows the distribution of widebody freighters by category of airline and by the region in which airlines are domiciled. The categories of airline used in this analysis are combination carriers (that is, carriers such as Lufthansa, Cathay Pacific, etc., that operate both passenger and freighter aircraft); express carriers (DHL, FedEx, etc.); scheduled-service all-cargo carriers (e.g. Cargolux and AirBridgeCargo Airlines); and specialist all-cargo carriers (e.g. Atlas Air and Air Atlanta Icelandic). Note that members of the specialist group operate most of their freighters on an ACMI or CMI basis in support of combination and express carriers. In recent years this has started to change, however, as specialist carriers have increasingly begun operating large widebody freighters for combination carriers and even scheduled all-cargo carriers. Atlas Air, for example, now operates 747s on an ACMI or CMI basis for clients such as Asiana, Cathay Pacific, and Nippon Cargo Airlines.

Several interesting factors become apparent when examining how widebody freighters are used:

While only 61.9% of the medium-capacity widebody freighters are operated today by express carriers, an overwhelming majority of the medium widebody freighters on order are bound for express carriers. The share operated by specialist carriers continues to grow, from 21% last year to 23.2% this year, primarily from the growing number of freighter-converted 767Fs operated by specialist carriers on behalf of Amazon Air.

Despite new large-capacity freighter deliveries to combination carriers including Turkish Cargo and Qatar Airways in 2018, the in-service ratio of large widebodies operated by combination carriers continues to fall, from 36.3% last year to 35% this year. Nearly half of the large widebody freighters currently in service, some 49.6%, are operated by or on behalf of express carriers. With the majority of the 747-8F and 777F backlogs destined for express carriers, this trend is set to continue.

See also: The widebody freighter fleet by carrier

On an overall basis, taking into account both the medium- and large-capacity freighter types, express carriers have a 46.3% share of the global widebody freighter fleet, versus 23.4% for combination carriers, 9.6% for scheduled-service all-cargo carriers and 20.7% for specialist all-cargo operators. But again, we note that many of the ACMI operators fly for express companies.

More than 70% of the medium widebody freighters are operated by airlines based in North America, nearly all by, or in support of, the integrators and, more recently, for Amazon. This is up slightly from last year, and future deliveries indicate the North American share will increase going forward. FedEx, UPS, and the airline subsidiaries of Air Transport Services Group and Atlas Air Worldwide Holdings are the main operators.

North America-based carriers operate 44.6% of the large capacity widebody freighters (up from 43% last year and 40% the year prior), while Asia-Pacific carriers have a 23% share, down from 28% just two years ago. The main differentiator between large-widebody fleets operated by carriers in North America versus those in Asia is the operator type. Most of the large widebodies in North America are operated by express or ACMI carriers, while most of those in Asia are operated by combination carriers. This too, is starting to change as Asian integrators, such as SF Express, develop an appetite for large widebodies.

{kind=link}