Passenger cap reduction puts $1B worth of Australian air trade at risk each month

Australian air freight exporters and importers may struggle to access already tight airfreight capacity when the reduction of international passenger arrival caps goes into effect July 14. The 50% reduction — from 6070 arrivals per week to 3035 — will likely lead to a proportional reduction of flights and airfreight capacity on them.

The planned extra repatriation flights into Darwin are unlikely to help since payload constraints will lead to little available capacity, and the routings are unlikely to be attractive for shippers. Australian importers and exporters could lose around 20% of the capacity currently available to them. Most importantly, this puts at risk close to AU$1.3 billion in Australian air freight exports or imports for every month the lower cap applies.

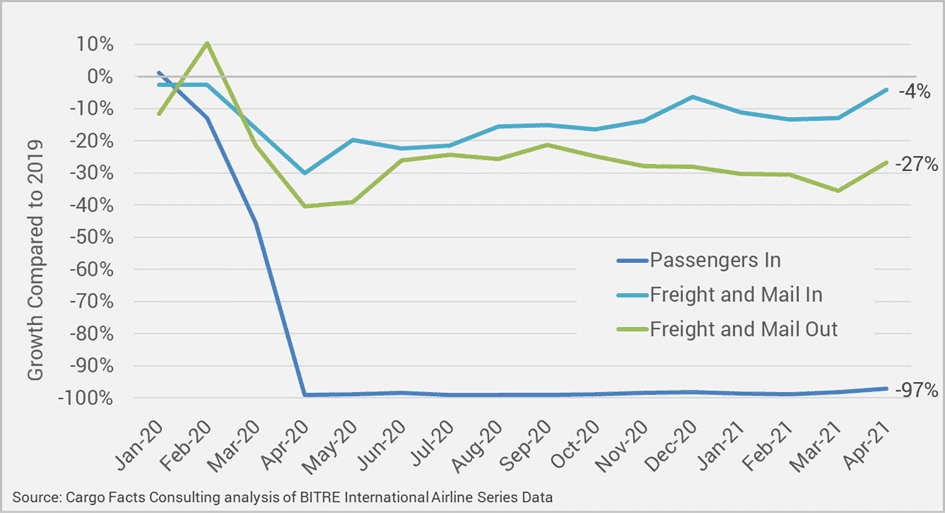

While airfreight volumes have seen a reduction during the past year, the decline has been nowhere near that of passenger volumes since Australia closed its borders on March 20, 2020. Last year, Australian international airfreight volumes declined by 19%, while passenger arrivals dropped by 97%. By contrast, the number of long-haul flights operated was down 73%.

Based on the most recent data shown here in Figure 1, April 2021 Australian inbound airfreight was running at about 4% below 2019 levels, while outbound freight was 27% below 2019 levels; this equates to about 40,000 tonnes into the country and 30,000 out. Passenger volumes continue to be only about 3% of their normal levels. Normal inbound passenger volumes are about 1.8 million a month, well below the 20-25,000 per month we have been seeing for more than a year.

Figure 1 – Australian Passenger and Air Cargo Volumes in 2020 and 2021 compared to 2019

While the share of airfreight traveling in the bellies of passenger aircraft is normally around 50% worldwide, about 80% of Australian airfreight normally moves on passenger aircraft. Most major freighter operators prefer to operate their equipment on more lucrative markets between Asia and North America, Asia and Europe, as well as between Europe and North America. Freighter operations to Australia tend to yield lower levels of profitability and also require aircraft and crews to be away from bases longer, leading to greater operational complexity and risk.

To compensate for the loss of freight capacity following large-scale flight reductions, the Australian government in April 2020 initiated the International Freight Assistance Mechanism (IFAM), a subsidy scheme designed to offset pandemic-induced rate increases and encourage carriers to fly capacity into Australia. The initial AU$110 million earmarked for the scheme was topped up four times: to AU$241.9 million in July 2020, $317.1 million in October 2020, and a further AU$112.8 million in March 2021. The latest top-up, which extends the scheme to September 2021, brings the total amount to AU$781.8 million. The newly imposed arrivals cap will likely see the requirement for a further top-up to guarantee exporters’ capacity requirements.

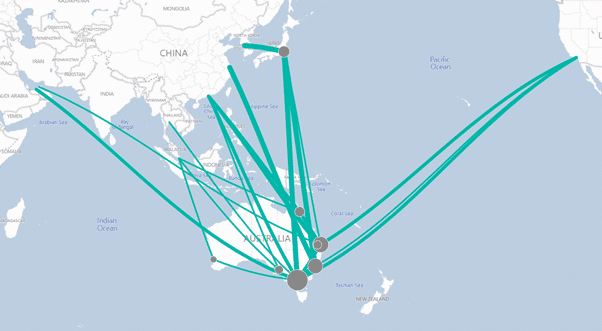

Figure 2 provides an overview of the routes provided by the nine airlines participating in the scheme. Currently, there are roughly forty-two flights per week, which offer subsidized capacity to exporters to the U.S., North and Southeast Asia and the Gulf. About half of the flights are operated by Qantas and about 20% by Japan Airlines. Singapore Airlines, Air New Zealand, Cathay Pacific, Emirates, Etihad and United Airlines also participate in the scheme. Qatar Airways participated in the IFAM earlier but has since pulled out.

Figure 2 – IFAM Flights as of 26 June 2021 (Source Australian Trade and Investment Commission)

Around 700 flights were operated into Australia in April 2021 from origins excluding New Zealand. If half of this capacity disappears, Australian exporters and importers could lose 20% of the capacity available to them, or about 7,000 tonnes per month in each direction. This could affect close to AU$1.3 billion in Australian air freight exports or imports.

{kind=link}