August US air imports signal recovery

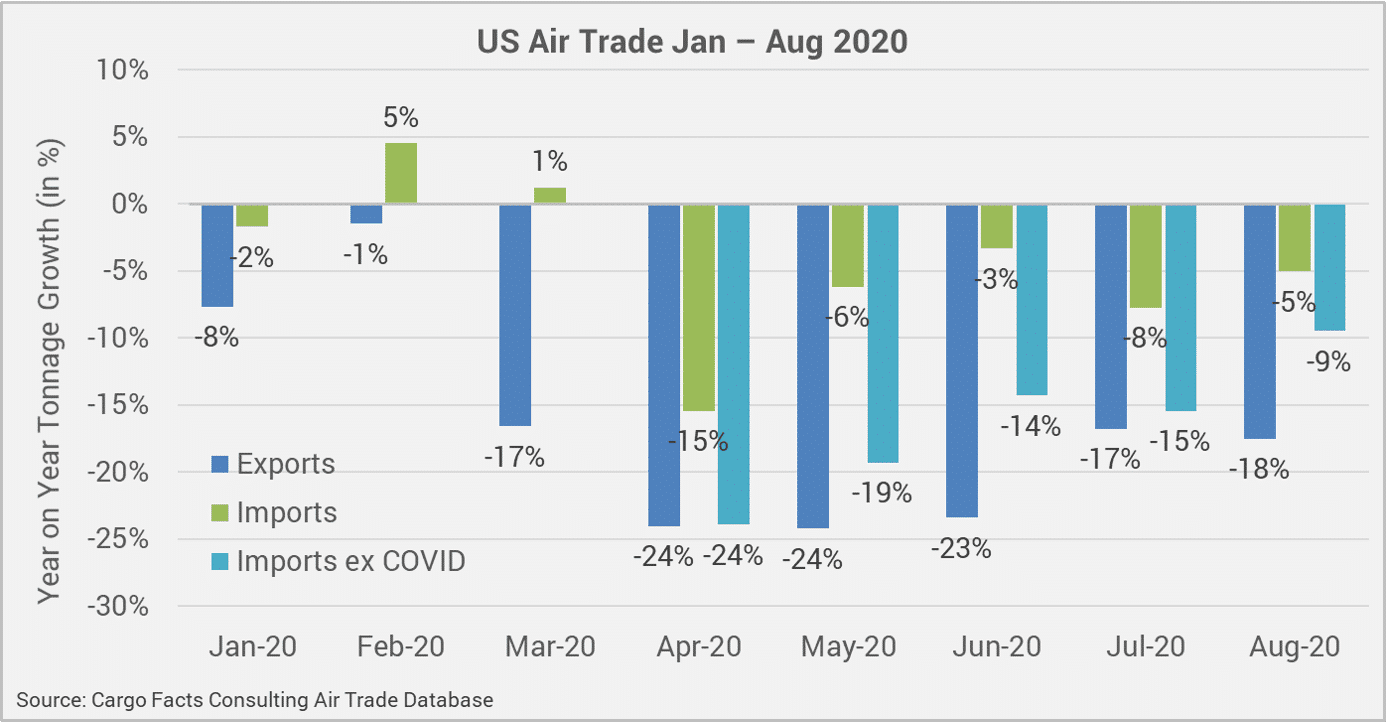

As it stands, U.S. air export and import tonnes are down 17% and 4%, respectively, for the first eight months of this year. Without the boost from COVID-related commodities, U.S. air imports would have been down 10%. That is bad, but the latest August figures show signs of recovery, and some product groups have done rather well this year.

While exports are still down significantly (17%-18% in the last two months), the decline is not as severe as in the second quarter. The rate of decline for imports has been slowing. In August, imports excluding the impact of COVID-related commodities were down 9%.

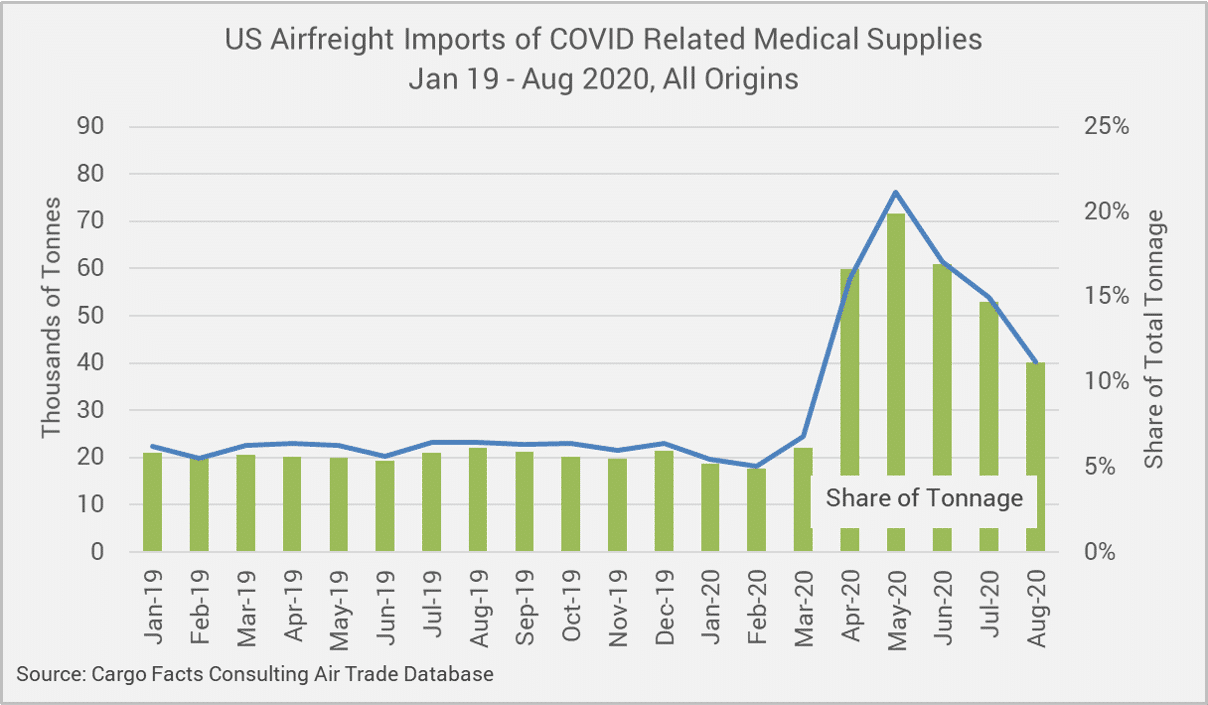

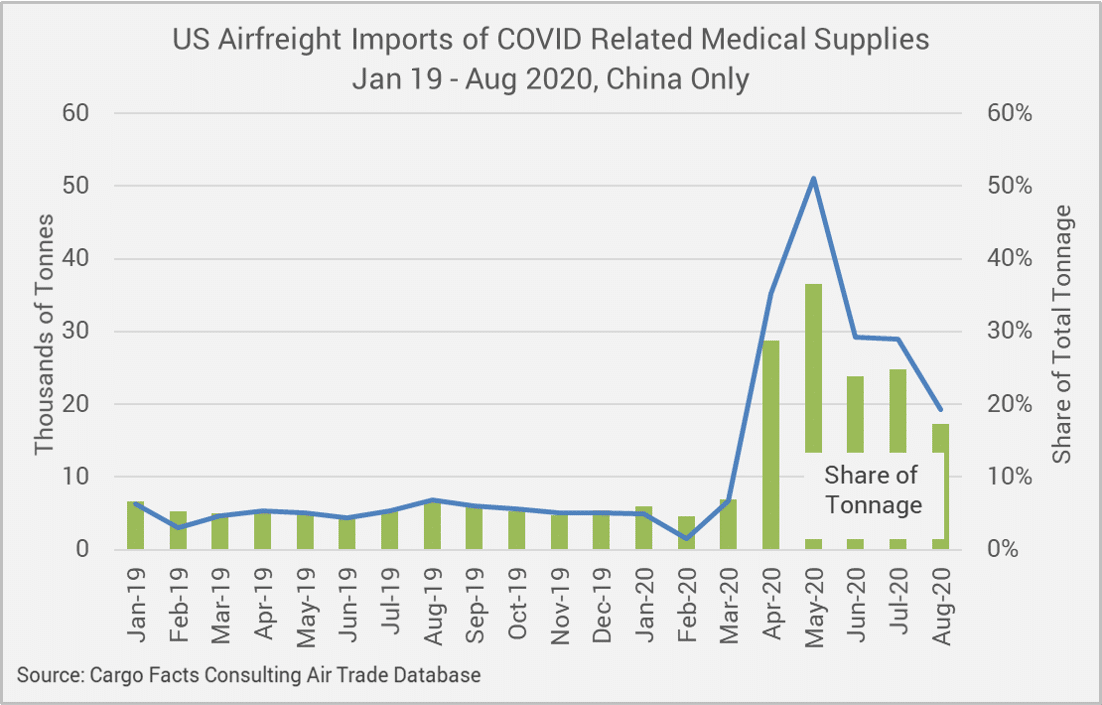

COVID-related commodities are still driving air freight import volumes, but this type of traffic is taking a smaller share of overall air import tonnage, down to about 10% of overall imports and less than 20% of air imports from China.

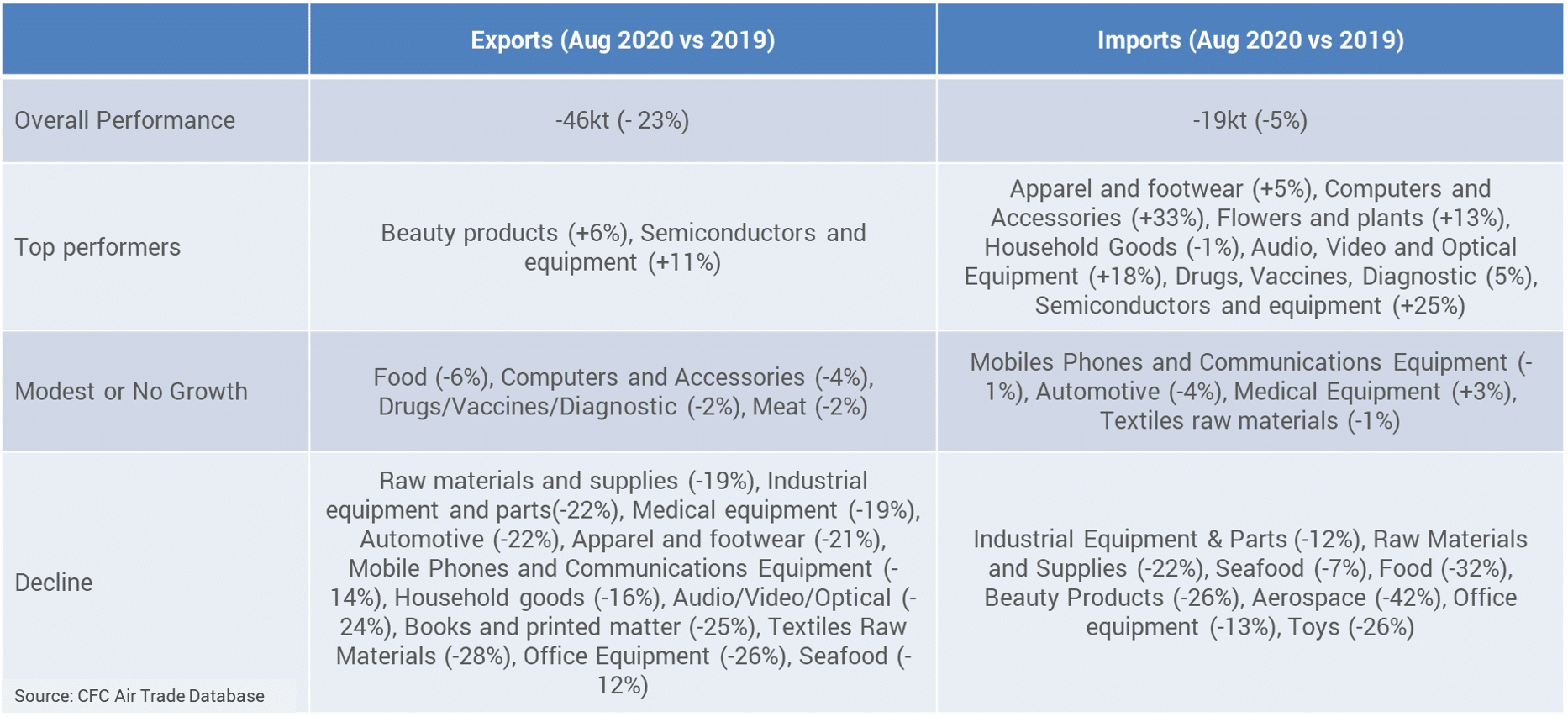

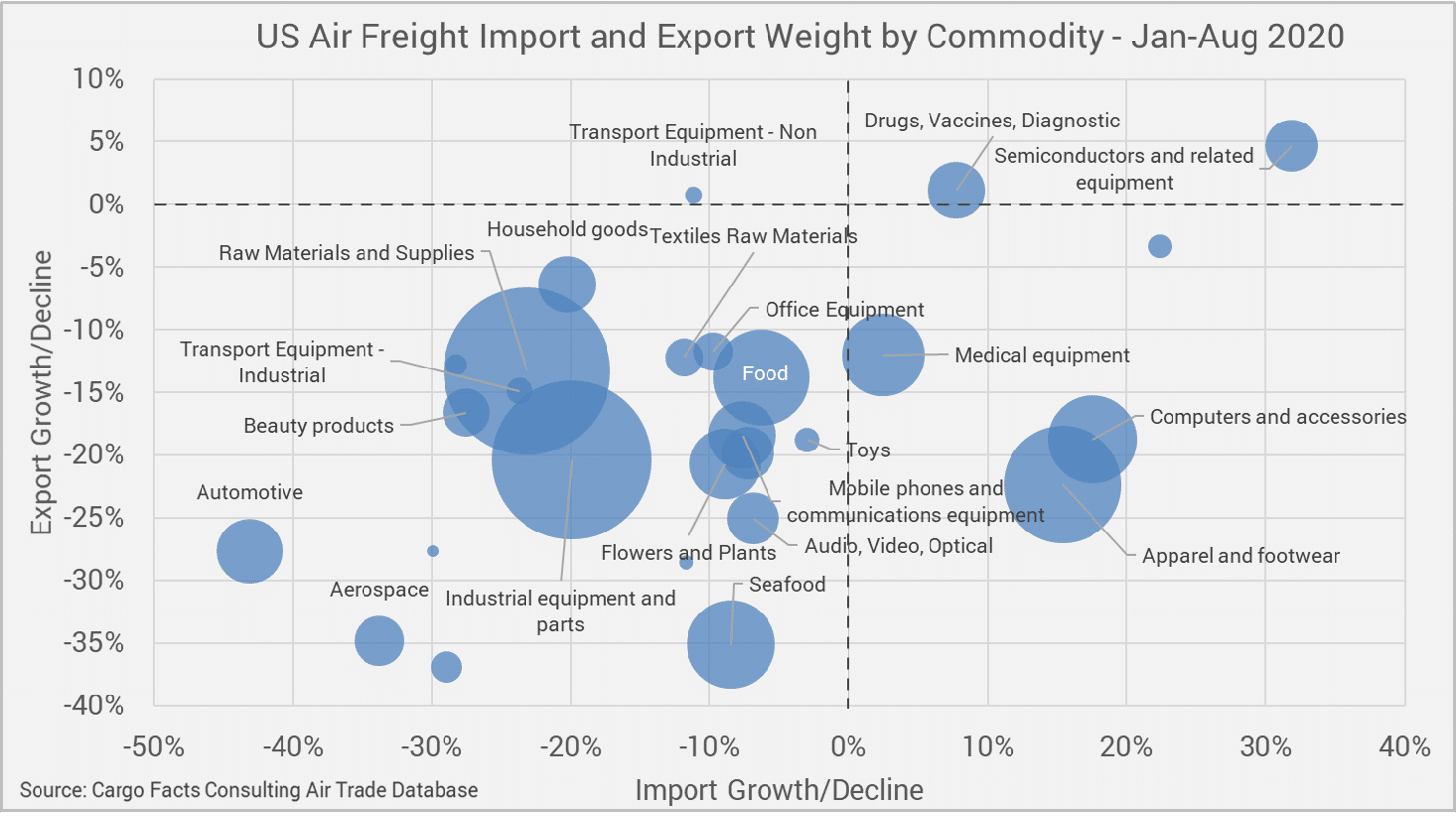

Apparel and footwear imports have been up throughout the pandemic but are primarily driven by PPE traffic currently, so the figure is not representative of what is happening in that market. However, computers, accessories, semiconductors and related equipment imports have been in year-on-year growth territory for the last six months. Unsurprisingly, imports of medical equipment and pharmaceuticals have also done well. While automotive imports are not looking as bad anymore, automotive exports are still way down. The table below shows developments by commodity in August.

During the course of the year most, but not all, product groups have registered declines on both the import and export side. Down significantly, in particular, are raw materials and supplies, and the industrial equipment and parts that are the staple of air cargo traffic and account for a third of all traffic. Computers, medical equipment, apparel (including PPE) are up on the import side. Only semiconductors and related equipment are showing growth on both the import and export side.

{kind=link}