No products in the cart.

Cargo traffic declined in January

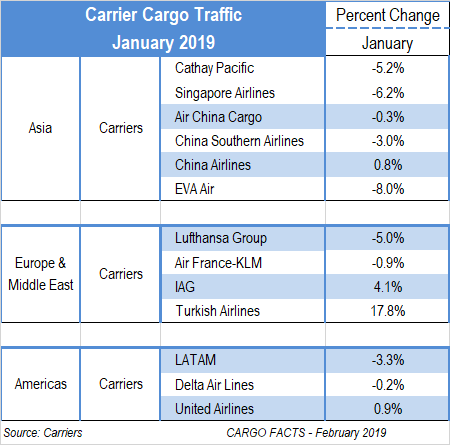

Almost unanimously carriers headquartered in Asia, Europe, and the Americas have begun reporting lower year-over-year cargo traffic for the month of January 2019. As can be seen from the chart at right, of the six major Asia-based carriers that have reported January traffic figures, all but one – China Airlines – have reported year-over-year declines in January ranging from between 0.3% and 8.0%. In Europe, results were mixed. Turkish Airlines reported double-digit year-over-year growth, while IAG Cargo saw traffic up a healthy 4.1%. This preliminary result follows on the back of two years of strong January growth. Most carriers reporting drops this year reported low-single-digit growth in both 2016 and 2017.

Almost unanimously carriers headquartered in Asia, Europe, and the Americas have begun reporting lower year-over-year cargo traffic for the month of January 2019. As can be seen from the chart at right, of the six major Asia-based carriers that have reported January traffic figures, all but one – China Airlines – have reported year-over-year declines in January ranging from between 0.3% and 8.0%. In Europe, results were mixed. Turkish Airlines reported double-digit year-over-year growth, while IAG Cargo saw traffic up a healthy 4.1%. This preliminary result follows on the back of two years of strong January growth. Most carriers reporting drops this year reported low-single-digit growth in both 2016 and 2017.

We note that any major fluctuation early in the year comes with the caveat that the timing of the Lunar New Year throws annual comparisons out of balance. This year, the holiday period came earlier in the year (5 Feb.), which could push volumes into February. The true picture will not emerge until year-to-date results are available at the end of February.

Regardless, this “first look” does not allay fears that increased headwinds from Brexit and the ongoing trade war between North America and China are starting to dampen global trade activity and air cargo volumes.

Turning to the individual results:

Asia Pacific

Cathay Pacific Airways reported January cargo traffic down 5.2% y-o-y to 904 million RTKs. This is the third consecutive month in which Cathay has reported year-over-year drops in cargo activity. Cargo and mail tonnage was down 3.4% at 167,000 tonnes. Commenting on the January performance, Director of Commercial and Cargo, Ronald Lam, said: “Chinese New Year this year was earlier than last, leading to a slight distortion in both passenger and cargo revenue for January and February. Cargo uplift gradually picked up before Chinese New Year, but the pre-holiday rush was not as strong as last year. As a result, our cargo revenue recorded small negative year-on-year growth in January. Some short-term capacity rationalization was made to better match demand.”

Singapore Airlines reported January cargo traffic down 6.2% year-over-year to 548 million FTKs on cargo volumes that were nearly flat (up 0.3%) at 106,000 tonnes. Cargo load factors dropped 3.8% to 58.1 points. Commenting on the results, the carrier said in a statement, “All route regions registered declines in CLF as demand did not keep pace with capacity changes.”

Beijing-based Air China reported January cargo traffic that was nearly flat with January 2018 (-0.3%) at 404 million RTKs, apparently accounting for disruptions stemming from the Lunar New Year Holiday. In a direct comparison between January 2019 and the year prior, Cargo Facts calculated cargo traffic (as reported) dropped 31% y-o-y, from 556 million FTKs in January 2019. Domestic traffic, meanwhile, grew slowly – up 1% y-o-y to 144 million RTKs.

Guangzhou-based China Southern Airlines reported cargo traffic down 1.4% year-over-year in January 2019, to 644 million RTKs, on weaker international traffic that was down 4.8%, to 479 million RTKs. Growth in China Southern’s domestic cargo business, which reported traffic up 10.6%, to 163 million RTKs, helped to lessen the blow.

Taiwan-based EVA Air reported an 8.0% y-o-y decline in traffic for January, to 297 million FTKs – the steepest drop in traffic for the carrier since 2016. Tonnage also declined 6.2% to roughly 53,000 tonnes. Taiwan Dollar-denominated (TWD) cargo yields, meanwhile, were up 10.3% y-o-y.

Taiwan-based China Airlines was one of the few carriers in the Asia-Pacific region to report growth in January cargo traffic, even if it was just slight growth – up 0.8% y-o-y to 436 million RTKs. Yields rose 10.4% y-o-y, to 7.8 TWD/FRTK. Cargo revenues continue to make up about 30% of China Airlines’ overall revenues.

Europe & Middle East

Air France-KLM reported overall group cargo traffic down 1.0% y-o-y, to 656 million RTKs, in January on weaker KLM Cargo traffic that was down 3.1%, to 371 million RTKs. Air France saw cargo activity increase 1.9% to 286 million FTKs.

International Airlines Group reported January cargo traffic up 4.1% y‑o‑y, to 449 million RTKs, on increasing cargo activity at the Group’s subsidiary carriers Aer Lingus and Iberia, which reported January traffic up 40% and 12.3%, respectively – albeit from low bases. British Airways saw traffic rise 1%, to 343 million RTKs.

Lufthansa Cargo Group airlines reported January traffic down 5.0% y-o-y, to 767 million RTKs. On a regional basis, Group cargo traffic was up 9.2%, to 62 million RTKs, on the Middle East/Africa lane, but these gains were not enough to offset a 9.2% drop in cargo traffic on the Asia-Pacific lane, to 343 million RTKs. Traffic on the America and Europe lanes also dropped 2.1% and 6.1%, respectively.

Turkish Cargo reported FTKs up 17.8% y-o-y in the first month of 2019 compared to January 2018. The carrier continues to outperform market growth as it continues to expand its freighter fleet, and continues to boost cargo in a growing number of markets.

Americas

LATAM Airlines Group reported January cargo traffic down 3.3% y-o-y, to 285 million RTKs, the carrier’s fourth consecutive month of lower traffic in annual comparisons with 2018. Load factors, meanwhile, dropped 1.1 pp, to 52.3%.

Delta Air Lines reported January cargo traffic down slightly (-0.2%) y-o-y to 226 million RTKs.

Those interested in learning more about the impact of the trade war, and where the market is headed for the remainder of the year, are invited to join us at Cargo Facts Asia 2019, to be held 15-17 at the Langham Shanghai. For more information, or to register, visit www.cargofactsasia.com. Discounted early-bird registration ends 1 March.

{kind=link}