No products in the cart.

Express companies attempt to shift from serving as mere e-commerce delivery subcontractors

In mid-September, Cargo Facts Consulting will publish a new report, the Global E-Commerce Logistics Outlook, to help companies craft their strategies towards a segment that has become increasingly important in logistics. This is the third of a series of articles leading up to the publication of the report that provides a window into our research. The first article focused on the logistics strategies of major e-commerce platforms and the second looked at how e-commerce has changed the nature of the postal business.

Express companies have traditionally played an important role in the distribution of e-commerce in both their intraregional and cross-border networks. Cross-border e-commerce revenues are only about a fifth the size of e-commerce in domestic markets, but are growing at a much faster rate as consumers become more comfortable buying items abroad and fulfillment chains improve.

However, integrators risk being cut out of large parts of the business that they helped to build up as e-commerce platforms insource their regional distribution networks, and as postal companies become more active in cross-border fulfillment, Cargo Facts Consulting research finds. Furthermore, the growth of e-commerce platforms with own-controlled fulfillment networks is creating potential competitors for the big integrators. With its own parcel network open to the general public, JD.com and Otto are the furthest in terms of creating their own integrated platforms. The big integrators all acknowledge this but their strategies to deal with the threat are still evolving.

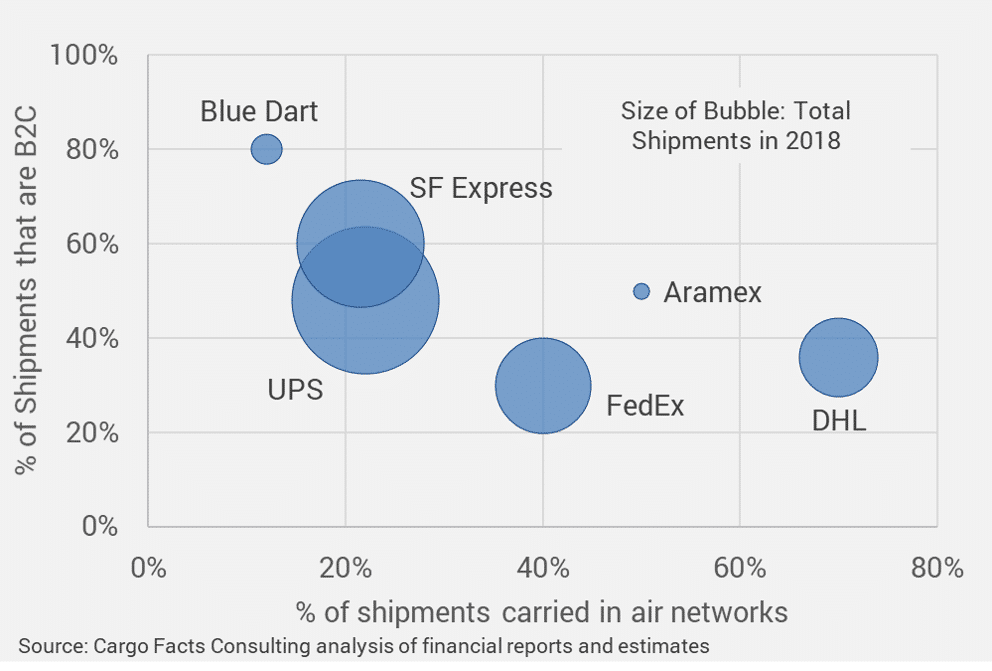

In their financial filings and reports, all integrators point out that growth in business-to-consumer traffic is a core part of their growth strategies. E-commerce traffic has become hard to ignore. Across the express business, the share of business-to-consumer shipments that is increasing faster than business-to-business shipments currently stands at approximately 48% of shipment volumes. The figure below provides an overview of the share of business-to-consumer traffic moving in major express carrier networks in relation to the air share of all shipments. The express operators below moved a total of over 13 billion shipments in 2018. As a rule, the bigger the ground network, the larger the share of business-to-consumer shipments.

Express Carrier Share of B2C vs Share of Shipments Carried by Air

According to Cargo Facts Consulting research, increasing e-commerce package traffic has been positive for utilization of sort facilities and both air and ground linehaul networks, but is increasing last-mile delivery costs due to the requirement to deliver lower-yield shipments to locations with lower population density. Moreover, the increase of business-to-consumer traffic in express networks has seen a decline of revenues per package, particularly in domestic networks.

Express carriers have realized that wholesale changes to their business models will be necessary to be successful in the future. These require a mix of actions that both increase and reduce cost. This includes service expansion to cater for seven-day deliveries and six-day pick-ups, investments in infrastructure and technology, while at the same time establishing lower-cost last-mile delivery channels through retail points and parcel lockers. As the focus shifts away from being mere servants to the big e-commerce platforms, the integrators are renewing their efforts to serve their traditional small and medium-sized business customer base. This effort may not be enough as the sheer scale of the big e-commerce platforms makes them hard to ignore. The 12 platforms covered in our forthcoming report account for 44% of global e-commerce revenues, most of which are generated via Alibaba, Amazon and JD.com.

Frederic Horst is Managing Director of Cargo Facts Consulting. He can be contacted by clicking here.

The Cargo Facts Consulting Global E-Commerce Logistics Outlook will cover the development of both domestic and cross-border e-commerce and its effect on multiple segments, including air cargo and contract flying, express, postal, and ground networks including last-mile delivery services. It will also take a detailed look at evolving fulfillment and logistics strategies of key global and regional e-commerce platforms, as well as at the relationships that are developing between different parties in the e-commerce value chain. The report discusses how companies are positioning themselves to benefit from year after year of double-digit e-commerce growth. In addition to detailed logistics profiles of the 12 most important global and regional e-commerce platforms, the report also contains e-commerce profiles of DHL and its Indian subsidiary Blue Dart, FedEx, UPS, SF Express, EMS/China Postal Airlines and Aramex. See www.cargofactsconsulting.com for details.

{kind=link}