Absent the bellyhold, freighter fleet can’t handle cargo demand

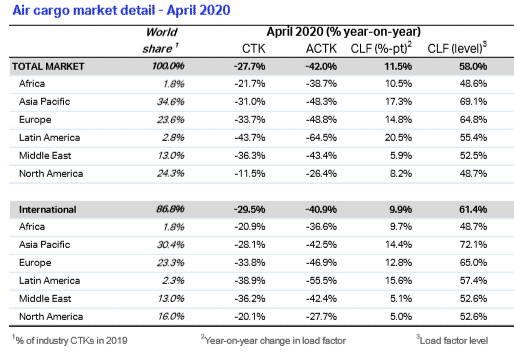

The International Air Transport Association released its airfreight market analysis for April 2020, showing a 27.7% year-over-year drop in worldwide cargo traffic, measured in cargo tonne kilometers (CTKs), the steepest decline ever to be recorded by IATA. Traffic was lower not only as a result of weakening underlying demand from industrial sectors, but in response to the precipitous drop in capacity, which was down 42% YoY.

With the COVID-19 pandemic affecting every major trade lane by April, international belly capacity was reduced by 75% compared to the previous year. Additional freighter and passenger-freighter flying increased capacity by a mere 15%, suggesting, “there is significant demand for air cargo which cannot be met owing to the cessation of most passenger flights,” according to IATA.

The capacity crunch drove yields higher on nearly all major routes. Although recent evidence suggests the peak may have passed, spot rates on the China-U.S. trade lane rose from just above $7 per kilogram at the beginning of April, to nearly $12 per kilogram by the end of April, according to the TAC Index.

Traffic and capacity were negative in every region, though the difference in magnitude was stark. Carriers based in North America recorded total market CTKs down just 11.5% YoY on capacity that was 26.4% lower. The large integrator fleets based in North America and the widespread use of passenger freighters by carriers based in the region returned to the market capacity that had been sapped from the bellyhold of passenger flights. African carriers also saw less-severe declines with total cargo traffic declining 21.7% YoY in April.

Latin American carriers saw the largest drop in capacity, with ACTKs down 64.5%, pulling traffic down 43.7% YoY. Two of the region’s largest, Santiago-headquartered LATAM and Colombia-based Avianca, filed for bankruptcy last month.

Carriers based in the Asia-Pacific region posted steep total traffic declines of 31% on capacity that was 42% lower. Some routes were less-severely impacted. The largest trade lane by CTKs, between Asia and North America, clocked traffic that was lower by just 7.3%, buoyed by higher PPE exports out of China.

Operators in the regions Europe and Middle East came out in the middle with total market declines of 33.7% and 36.3% respectively in April.

Year-to-date total market FTKs are down 12.7% YoY.

{kind=link}

Cargo Facts Free Newsletters