Far from stellar, Lufthansa Cargo questions if 2019 will be a normal year, or a crisis year

FRANKFURT, Germany – After two stellar years of growth for air freight, increasing trade friction is making Lufthansa Cargo feel more cautious about its outlook for 2019. Long-term, however, the German combination carrier maintains a positive outlook and continues to invest in its freighter fleet and cargo infrastructure.

At its annual press conference in Frankfurt on 18 March, CEO Peter Gerber emphasized the uncertainties surrounding the near-term outlook, with air cargo markets contracting on a large scale for the first time since early 2016. Although medium-term indicators for the global economic outlook, such as population and income growth, remain strong near-term, the market will be strongly affected by trade conflict and geopolitical issues, he said. Despite being just days away from the execution of a no-deal Brexit, the carrier did not foresee any impact resulting from the chaos surrounding the United Kingdom’s pending departure from the European Union.

Despite the prospective market turmoil, CFO Martin Schmitt confirmed that LH Cargo’s fleet modernization plans will continue into 2019 as incoming 777Fs replace aging MD-11Fs. In parallel, the Group’s subsidiary carrier, AeroLogic (a 50/50 JV with DHL Express), also continues to expand its freighter fleet, which currently includes eleven 777Fs. This year, the Group will add a total of four 777Fs, half of which will be flown by AeroLogic. Two of the aircraft have already been delivered – one each to Lufthansa Cargo and AeroLogic. Lufthansa Cargo’s second 777F is due in a couple of weeks. AeroLogic, meanwhile, added a 777F in January and expects an additional unit next fall.

Lufthansa Cargo currently operates twelve MD-11Fs and six 777Fs, following the carrier’s latest 777F delivery in February. Of the twelve MD-11Fs currently operating in the carrier’s fleet, two will be phased out by yearend 2019, and have already been sold. Cargo Facts expects the MD-11Fs will migrate across the Atlantic and will end up in the fleet of Western Global Airlines – as has been the case with four of LH Cargo’s previous MD-11F retirements.

As for the ten remaining MD-11Fs in Lufthansa Cargo’s fleet, the carrier confirmed it is still on track to phase out the aircraft type entirely by 2025. It is worth noting that the low remaining book value of its MD-11 fleet gives Lufthansa Cargo ample flexibility to deal with any potential market downturn. If no further MD-11Fs are retired, the additional 777Fs will boost the Group’s cargo capacity, but at a rather conservative pace. Last year, overall capacity increased by 5%, but freighter capacity grew only 1%. This is likely to increase slightly in 2019 as 777Fs are added. The new 777 freighters to enter the fleet this year are expected to be deployed on trunk cargo routes such as Chicago, Atlanta, and Tokyo.

Despite AeroLogic and Lufthansa Cargo being based in different cities, the 777Fs being added this year are expected to operate out of Frankfurt, as the company does not see much business potential for general freight out of Leipzig. For the foreseeable future, Lufthansa Cargo’s focus remains on Frankfurt, even though the company admitted that the night flight ban costs the company approximately €40 million per annum. Lufthansa is in the process of planning a major €400 million overhaul to its Frankfurt Cargo Center and expects the refreshed facility, to be built on the footprint of the existing facility, to be completed by 2024.

Apart from freighter capacity, changes to the passenger fleet and network of Lufthansa’s network carriers also boosted capacity. A few notable 2018 capacity developments include:

- LH Cargo completed the integration of Brussels Airlines’ bellyhold capacity and increased connections to Africa.

- Lufthansa replaced A340s with cargo-friendly A350s in Munich.

- Eurowings added new destinations to Asia and North America.

In addition to its own network, partnerships continue to be a major focus for Lufthansa Cargo. The carrier expanded cooperation with Cathay Pacific, entered into a new alliance arrangement with United and, continues to share capacity with All Nippon Airways (ANA). The company did not provide any further commentary on its recently launched joint operation with China Post, but did indicate that a launch of a specialized e-commerce product was imminent.

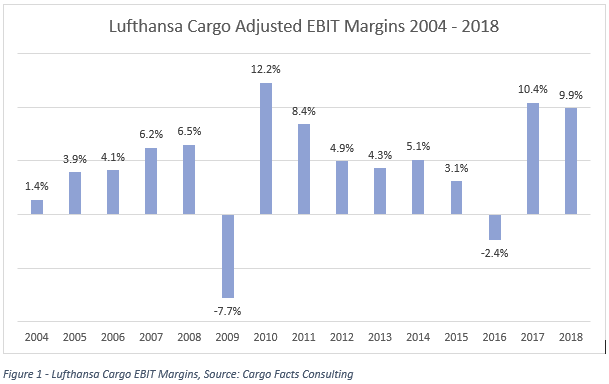

Turning now to results, for the full-year 2018, Lufthansa Group’s Logistics Division (Lufthansa Cargo) achieved an adjusted EBIT of €268 million on revenues of € 2.7 billion. Financially, 2018 and 2017 have been unusually good years for Lufthansa Cargo, with adjusted EBIT margins of 9.9% and 10.4%, respectively (see Figure 1). Last year’s figures were adjusted for changes in the accounting of engine overhauls.

While most of the Lufthansa Cargo’s profits came from its core operation, approximately €37 million of EBIT was related to its subsidiary investments, with the top performers being Pudong Air Cargo Terminals Ltd (PACTL) and time:matters. Overall Logistics segment Return of Capital Employed (ROCE) was 15% in 2018 and 16% in 2017, substantially higher than Lufthansa Group’s Weighted Average Cost of Capital (WACC) of just over 4%.

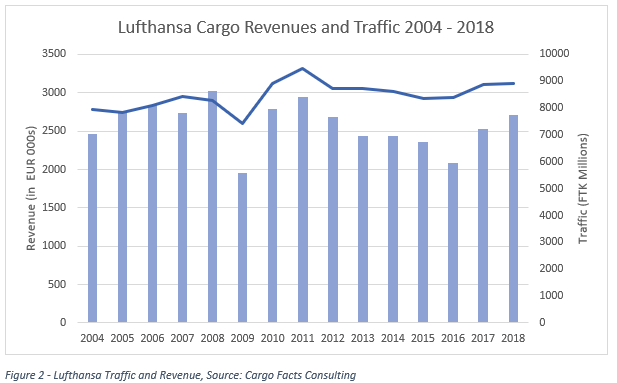

Revenue in 2018 was almost 8% higher than in 2017, but traffic and profits were only up 1% and 2%, respectively. While this was in line with guidance provided following third quarter 2018 results, it is below industry growth. Overall air cargo industry revenue growth in 2018 was closer to 14% off the back of traffic growth of 4%.

Last year’s traffic was only 8% higher than in 2008, which equates to an average annual growth of 0.8% (see Figure 2). In 2003, Lufthansa Cargo was still the 2nd largest cargo carrier worldwide, but has fallen down the ranking since then and currently stands at 6th place behind Cathay, Qatar, UPS, Emirates, and FedEx. However, when Swiss is factored in, then the group ranks on par with Emirates.

Most of Lufthansa Cargo’s growth in 2018 came from Asia-Pacific services, where revenues grew by 12%, mainly due to higher yields. Americas revenues increased by 6%, while Europe, Middle East, and Africa revenues were flat on reduced traffic volumes. Load factors declined by 3.2 pp network-wide, mainly due to the addition of additional belly capacity on routes with low freight demand.

However, despite an increase in fuel expenses of 16%, the company managed to reduce its unit cost by 0.4%. This improvement comes off the back of its “C40” program which saw expenses fall by €80 million following the reduction of one leadership layer and implementation of more efficient processes. C40 was implemented one year earlier than planned.

Looking beyond restructuring, further focus will be put on digitalization of processes in 2019, including the rollout of a fully automated spot pricing system, commencing development of a new booking engine.

Join us at Cargo Facts Asia 2019, 15-17 at the Langham Shanghai, where Frederic Horst will present the 2019 edition of Cargo Facts Consulting’s annual twenty-year Freighter Forecast. For more information, or to register, visit www.cargofactsasia.com.

{kind=link}

Cargo Facts Free Newsletters