Freighter distribution within the widebody fleet: Part I

Last month, Cargo Facts presented a detailed analysis of the widebody freighter fleets of airlines worldwide. The analysis showed that between 2018 and 2019, the widebody freighter fleet expanded by 7.1% as carriers adjusted capacity to meet growing demand for air cargo. As of mid-January 2019, seventy-six airlines operated 1,109 widebody jet freighters in commercial service and the backlog for production widebody freighters stood at 146 units.

Today we begin a two-part look at the way those 1,109 widebody freighters are operated and how the different types of widebody freighters are distributed within the fleet — by type, by manufacturer, by operator type, and by geographical region.

As air freight demand growth began to accelerate in mid-2016, growth to the widebody freighter fleet lagged behind. Marking a departure from recent years where the numbers of operators and units on order have been steadily falling, last year was different – the widebody freighter fleet swelled, as did the number of widebody operators, and the backlog.

In 2016 and 2017, carriers were reluctant to execute purchase orders for new production freighters, and the order backlog shrank even as air cargo demand grew. Following a resurgence in new orders in 2018, however, the backlog has increased by nearly 20%, to 146 units. Express carriers were primarily responsible for the swelling backlog with large orders from DHL, FedEx, and UPS placed in 2018.

In June, FedEx placed an order for twelve 777Fs (of which, seven were new orders and five were already on order but had not yet appeared in Boeing’s order book). The following month, DHL Express’ ordered fourteen 777Fs, with an option to take up to seven additional 777Fs.

Comparing the current fleet to the tally at the end of January last year on a model-by-model basis shows substantial increases for all three of Boeing’s current production freighter types:

- The 767-300F fleet increased by eighteen units to 146 (a 14% increase), all of which went to FedEx. Two additional 2018 orders for the airframe include a twelve-unit order from FedEx and a nine-unit order from UPS.

- The 777F fleet grew by fourteen units to 152 (10%). Three each went to FedEx, EVA Air, and Turkish Cargo, which received its first 777F in December 2017. Ethiopian Airlines and Qatar Airways each took delivery of two 777Fs, and Etihad Airways took delivery of one 777F.

- The active 747-8F fleet grew by seven units (9%) to eighty-three as Boeing delivered six 747-8Fs to UPS and Saudia Cargo reactivated a parked -8F. UPS firmed up options for fourteen additional -8Fs, and when combined with additional new and existing orders, boosted the 747-8F order backlog to twenty-five units.

In addition to the net of thirty-nine new production freighters, the resurgence in demand for medium widebody freighters that began three years ago continued in 2018, with the redelivery of twenty-two P-to-F conversions, including nine 767-300BDSFs, twelve 767-300BCFs, one A330-200P2F and an A330-300P2F.

Of course, there were retirements, too, although not as many as in the past. Over the past year, a net of eleven freighters of three types left the fleet, including six DC/MD-10-30Fs, four 767-200Fs and one A300-600F. Regarding the 747 Classics, there are two or three still in irregular charter service, mostly in the CIS region, but their impact on the overall air freight market is so small that we have chosen to disregard them.

However, in contrast to 2018, when carriers brought just three 747-400Fs into service, this year carriers brought fifteen widebody freighters back into service – six 747-400ERFs, two 747- 400BCFs, four 747-400BDSFs, three MD-11Fs, and two A300B4Fs.

New-build widebody freighters will continue to enter the fleet over the next few years, but the current backlog of 146 orders is well down from the 203 units on order just six years ago. Cargo Facts does not see any major resurgence in demand for the large widebody types next year as 2018 already witnessed record orders. Growth of the fleet depends on the extent to which the express companies, and the various carriers that fly for them, expand their medium widebody fleets with new-build 767-300Fs and freighter-converted A330-300s and 767-300s in order to keep up with the explosion of e-commerce.

FedEx ordered 119 767-300Fs from Boeing, but with more than sixty of those still to come, another big order seems unlikely. DHL, which operates fewer aircraft of its own than FedEx and UPS, has never shown much of an appetite for medium widebody production freighters, but that could change following its recent order for 777Fs. DHL has placed orders for eight freighter-converted A330-300s with EFW, and, barring some unexpected hitch in the development of the conversion program or the performance of the aircraft, will likely order more – but not on the scale of FedEx’s 767 order.

Which, among the big three, leaves UPS. In late 2016, UPS placed an order for fourteen 747-8Fs, and, last year firmed up options for fourteen more. But with the end of production of the 747-8F now on the horizon, further orders for the type – whether from UPS or anyone else – appear unlikely beyond a five-unit order from Volga-Dnepr Group announced at the 2018 Farnborough Air Show. UPS’ medium widebody fleet includes sixty 767-300Fs, two 767-300BCFs, and fifty-two A300-600Fs. At least one 767-300BCF and nine 767-300Fs remain in Boeing’s order backlog. As the A300-600Fs come up for replacement, additional medium widebody orders are likely on the horizon. UPS continues to operate thirty-seven aging MD-11Fs which it may consider replacing in the coming years, so a 777F order would not be surprising, but so far we have heard no indication that it is imminent.

Regarding the other potential customers mentioned above, both Amazon and SF Express are believed to have evaluated new-build 767 freighters, but to date, both companies seem content with conversions. Feedstock limitations, however, will inevitably push both companies towards production freighters, or a different operating platform, such as freighter-converted A330-300. Last year, ATSG secured rights to twenty 767-300s scheduled to come out of the American Airlines fleet over the next few years. SF Airlines had been competing fiercely for the feedstock, but lost the bid to ATSG.

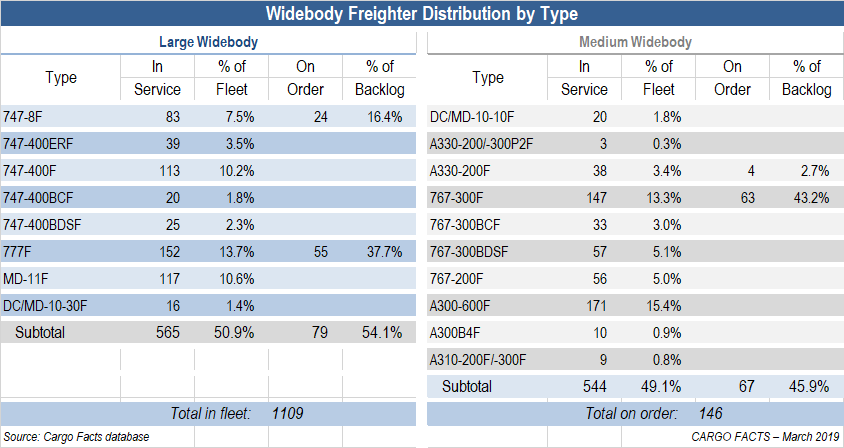

The chart at right summarizes the composition of the medium- and large-capacity widebody freighter fleets, reflecting both the 1,109 units that are in service today, and the 146 additional production units now in the order pipeline. Delivery of most of the freighters in this backlog will take place over the next three-to-four years, but aren’t expected to have a major impact on the retirements of MD-11Fs and 747-400Fs, at least in the near-term.

The chart at right summarizes the composition of the medium- and large-capacity widebody freighter fleets, reflecting both the 1,109 units that are in service today, and the 146 additional production units now in the order pipeline. Delivery of most of the freighters in this backlog will take place over the next three-to-four years, but aren’t expected to have a major impact on the retirements of MD-11Fs and 747-400Fs, at least in the near-term.

FedEx and UPS are adding widebodies to accommodate growth, rather than replace retiring aircraft. During the five-year fiscal period between 2019 and 2023, FedEx, for example, plans to add seventy-seven widebody freighters – sixty 767Fs, and, seventeen 777Fs – but will only retire twenty-three MD-10-10Fs, thirteen MD-10-30Fs and two 747-400Fs, according to its most recent Stat Book. Although some of FedEx’s leased A300-600Fs may be disposed of following their lease expiration, the carrier’s entire MD-11F fleet (fifty-seven units) is expected to fly beyond 2024. Similarly, when UPS firmed up options for fourteen additional 747-8Fs the company s, “All of the new aircraft will be added to the existing fleet and no existing aircraft are being replaced.

In terms of the composition of the fleet today, the continuing strong demand for the 767-300F pushed Boeing’s share of the medium widebody fleet to 56.1% last year, and that has increased to 57.5% this year. With outstanding orders for sixty-three 767-300Fs, as opposed to just four A330-200Fs, and the boom in 767-300BCF/BDSF conversions, Boeing’s share will continue to grow substantially over the next few years. There will come a day when growing demand for A330-300P2F conversions will slow this trend, but that day is still some way off.

Boeing continues to have the large-capacity freighter segment to itself. The in-service numbers reflect a growing quantity of 777 and 747-8 freighters and reactivated 747-400Fs and slight growth to the in-service freighter-converted 747-400s, and MD-11 and MD/DC-10-30 freighters.

The outstanding orders in the large capacity segment include twenty-four 747-8Fs (down from twenty-five last year) and fifty-five 777Fs (up significantly from thirty). The widebody production backlog of seventy-nine units is up from fifty-five last year.

Tomorrow in part II, we’ll continue the analysis with an overview of widebody freighter distribution by manufacturer, operator type and region.

Those interested in learning more about future demand for production freighters are invited to join us at Cargo Facts Asia 2019, to be held 15-17 April at the Langham Shanghai. For more information, or to register, visit www.cargofactsasia.com.

{kind=link}

Cargo Facts Free Newsletters