E-commerce traffic boosts US domestic air express outlook through 2026

E-commerce is lifting growth expectations for the United States’ domestic air express market, already the world’s largest, according to a forecast from Cargo Facts Consulting.

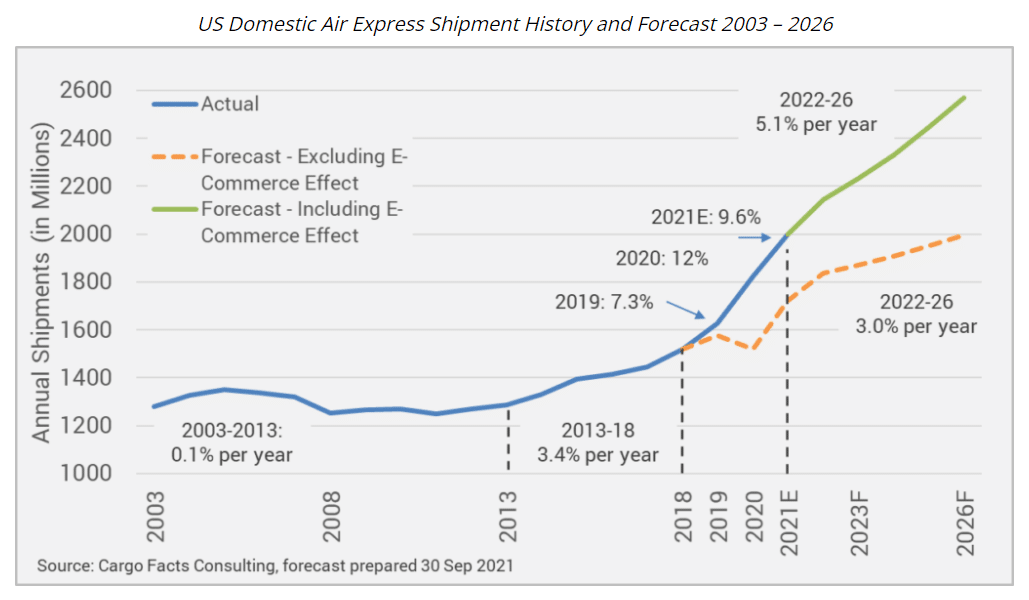

CFC predicts the market will grow by just under 10% this year, and then moderate to an average of 5.1% per year for the next five years.

Excluding the effect of online shopping moving through express networks, growth would be closer to 3% per year.

The domestic U.S. air market is on track to hit 2 billion shipments in this year with FedEx and UPS together accounting for about 50% to 55% of domestic revenue freight-ton-miles. Their share has been decreasing primarily as a result of Amazon’s dedicated network, which will include more than ninety aircraft operating in North America by the end of this year.

The chart below provides an overview of Cargo Facts Consulting’s most recent analysis of air express shipment traffic, as well as a forecast through to 2026.

Cargo Facts Consulting defines “air express” as the market for overnight and deferred shipments but excludes ground operations. In comparison, the combined ground operations for FedEx and UPS move more than four times the volume of shipments moved by air. Also included is UPS express mail operations, but since the departure of DHL from the U.S. market in 2008, the market is essentially a duopoly between FedEx and UPS. Amazon Air’s in-house operations are excluded as CFC considers them to be an intra-company fulfillment network. Measured in flights however, Amazon’s air network is one-third the size of UPS’ and one-fifth the size of FedEx’s.

Cargo Facts Consulting defines “air express” as the market for overnight and deferred shipments but excludes ground operations. In comparison, the combined ground operations for FedEx and UPS move more than four times the volume of shipments moved by air. Also included is UPS express mail operations, but since the departure of DHL from the U.S. market in 2008, the market is essentially a duopoly between FedEx and UPS. Amazon Air’s in-house operations are excluded as CFC considers them to be an intra-company fulfillment network. Measured in flights however, Amazon’s air network is one-third the size of UPS’ and one-fifth the size of FedEx’s.

As the chart indicates, the U.S. air express market has gone through a number of phases. From 2003 to about 2013, the market hardly showed any growth. Much of the volume that DHL left behind after its departure disappeared or began moving in ground networks. Between 2013 and 2018, growth picked up to an average of 3.4% per year as economic activity accelerated following the Great Recession. The air express market went into overdrive in 2018 thanks to rapid growth in e-commerce shipments requiring two-day and overnight delivery.

While e-commerce traffic had been increasing as a share of total shipment volumes for several years, 2020 provided an additional boost. “The spike in residential deliveries more than made up for the drop in business-to-business traffic dropped as large parts of the fixed retail business was closed,” said Frederic Horst, managing director of Cargo Facts Consulting. This traffic has remained strong throughout 2021 and business-to-business traffic has risen to pre-crisis levels.

FedEx recently predicted that the U.S. domestic package market would grow by 10% per year to 2026. CFC analysis, meanwhile, points to lower growth rates for the air express market. Most of the growth in the package market has been and is likely to be seen in ground rather than air networks. China illustrates this point well. A few years ago, SF Express was moving 18% of its traffic through its air network. Today that figure is closer to 10%. “Air Express networks are too yield-hungry for business-to-consumer e-commerce and densification of distribution center networks will see volumes increase more in last-mile than longer-haul networks,” Horst said.

Cargo Facts Consulting is in the process of updating its annual air express market outlook, which provides an in-depth look into the historical performance and outlook for the world’s major express companies DHL, FedEx, SF Express, UPS as well as regionally operating companies such as Aramex, Blue Dart, Toll and Estafeta, among others. The report also includes a forecast of domestic U.S., international and intra-European express volumes. The report will be published in late October or early November.

Cargo Facts Symposium, taking place LIVE Oct. 25-27 at the Wynn Las Vegas, is the essential event for stakeholders in the air cargo industry. Learn more and register at www.cargofactssymposium.com.

{kind=link}

Cargo Facts Free Newsletters