Freighter fleet analysis part I: European metal

Were “innovation” to be defined by a cargo airline’s propensity to add the latest production and conversion freighter models, airlines in Europe would do quite well. Unfortunately, that remains a rather unconventional way to define innovation. Still, over the course of 2018, carriers with European Air Operator Certificates (AOC) have surfaced as early adopters of next-generation freighter conversions for both widebody and narrowbody airframes. This year also witnessed an uptick in production freighter orders from European carriers, warranting a fresh look at the narrowbody and widebody freighter fleets currently in service across the continent, by carrier.

“Europe” for the purpose of this piece is defined as the fifty-one independent states delineated by the Ural Mountains in Russia, the Caspian Sea, and Caucasus Mountains. Using this definition allows for the inclusion of fast-growing airlines such as Turkey’s national carrier, Turkish Airlines, Azerbaijan-based Silk Way West Airlines, and Moscow-based AirBridgeCargo.

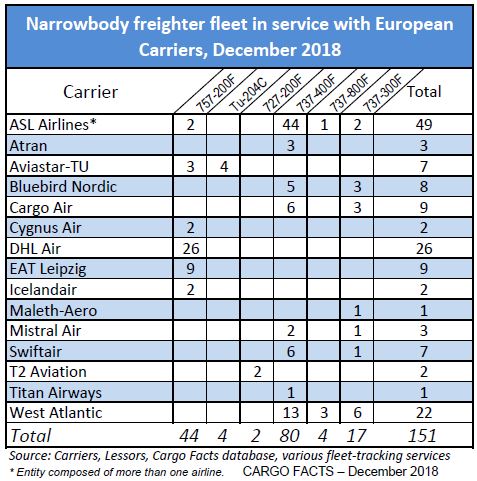

Beginning with the narrowbody freighter fleet in service with European carriers, the chart at right shows a total of 151 narrowbody freighters distributed among fifteen carriers and carrier groups across Europe (see note on groups below). At 64%, the majority of the fleet is in service with just three companies – ASL Airlines, DHL Air and West Atlantic. By a wide margin, the 737-400F is the most popular narrowbody freighter in service with European freighter operators, comprising more than half of the fleet at 53%. Combined with other variants, the 737Fs make up 67% of the total narrowbody fleet. The larger 757-200F is a distant second, making up just under 30% of the fleet.

As the new generation of conversions begins replacing older types, the 737-400F’s share of the overall European narrowbody freighter fleet will certainly fall, but at present, nothing threatens to rattle the overall dominance of the 737F. To date, European carriers have placed no firm orders for A320-family conversions – though, it should be noted that Luxembourg-based Vallair is the launch customer for the A321-200 P-to-F programs of both EFW and 321 Precision.

Joining the European freighter fleet for the first time this year is the 737-800BCF, which Boeing redelivered to launch customer GECAS in April. GECAS in turn leased the freighter to Sweden-based West Atlantic. As was the case for two additional -800BCFs West Atlantic has since added, the aircraft operate within FedEx’s European network. West Atlantic has agreed to lease at least one more -800BCF from GECAS.

No longer is West Atlantic the sole operator of the 737-800BCF and has since been joined by ASL Airlines whose Belgian subsidiary, ASL Belgium, took delivery of its first 737-800BCF on lease from GECAS in April. ASL has since taken delivery of a second freighter of the airframe type and has no further commitments with GECAS at this time. After taking redelivery of five -800BCFs, GECAS has a backlog of forty-five firm orders and options for conversions with Boeing and an additional twenty orders and options for AEI’s forthcoming -800 conversion.

Two other carriers that have made relatively significant fleet changes over the course of 2018 are Russia-based Aviastar-TU and Italy-based Mistral Air. In June of this year, Poste Italiane and Amazon signed a three-year agreement to facilitate e-commerce deliveries and returns in a deal that was in line with the Post’s broader five-year, “Deliver 2022” strategy, which aims to boost parcel revenues by 70% to US$1.41 billion over the next five years. To achieve this objective the post’s affiliate carrier, Mistral Air has added two 737-400Fs on-lease from Automatic LLC. Aviastar- TU, meanwhile, has branched out from Tupelov operations with the introduction of three 757-200Fs to its fleet.

Tally note: For the purposes of this article, tallies include freighters operating on an AOC of a carrier based in Europe, regardless of whether the aircraft is on operational lease or if the carrier is just providing CMI services. Where appropriate, fleet counts are reported by carrier group to reflect the aggregate number of aircraft in service across group subsidiary carriers. For example, “ASL Airlines” includes subsidiary carriers in Belgium, France, Hungary, and Ireland. Aircraft in Quick Change configuration are included if evidence suggests they are operated full-time as freighters. Less common types, such as the few remaining 707Fs and DC-8Fs, as well as freighters in combi configuration, are excluded.

Next week, part II of “European Metal” will examine the widebody freighter fleet in service with European carriers.

Those interested in learning more about the market for narrowbody freighters in Europe are invited to join us Cargo Facts EMEA, to be held 4-6 February at The Westin Grand Frankfurt. Register before 14 December to take advantage of early bird rates. To register or for more information, visit www.cargofactsemea.com.

{kind=link}

Cargo Facts Free Newsletters