Overall air cargo demand is flat, but certain pockets thrive

The 31-month streak of year-over-year increases in demand for air freight had to end sometime, and that time has now arrived, according to the latest roundup of November 2018 air cargo totals from IATA, as well as from cargo analysts WorldACD.

The 31-month streak of year-over-year increases in demand for air freight had to end sometime, and that time has now arrived, according to the latest roundup of November 2018 air cargo totals from IATA, as well as from cargo analysts WorldACD.

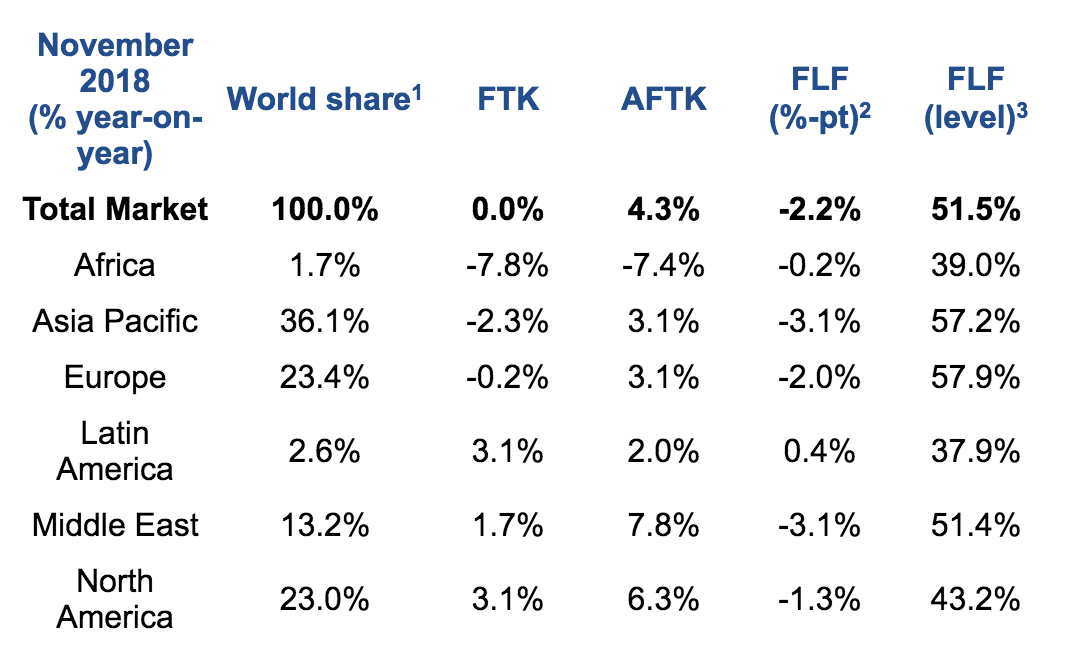

However, while the current trade environment and flat macro-economic averages portray a grim picture at first glance, the figures do not reflect a uniform pattern observable across the board. (See the table to see region-by-region data.)

IATA’s November data indicated that global growth volumes, on average, finally slowed to a flat zero, measured in freight tonne kilometers (FTKs), amidst a slower-than-normal peak season.

Protectionist policies likely contributed to stifled demand, especially along trans-Pacific and U.K.-E.U. trade lanes, which director general and CEO of IATA Alexandre de Junaic said remain a “cause for great concern.”

IATA noted that Europe’s slight dip in demand was also influenced by “weaker manufacturing conditions for exporters and shorter supplier delivery times, particularly in Germany,” a key export market in Europe.

But the hub of Germany’s western neighbor, Liege Airport (LGG), for instance, isn’t experiencing the slump. In fact, the airport just had its second record-breaking year in a row – today, reporting a 21.5 percent increase in cargo traffic, year-over-year, to 870,644 tonnes.

And it’s investing in future growth with the addition of 30,000 square meters of warehousing space for air cargo handlers in 2019, in light of new partnerships with Alibaba and AirBridgeCargo.

The regions of North America and Latin America are also still experiencing increased demand for air cargo – both showing that volumes increased by 3.1 percent, year-over-year, in November.

Looking ahead, despite concerns, IATA still expects growth between 2018 and 2019 – forecasting that cargo tonnes carried will reach 65.9 million in 2019, up from 63.7 million in 2018.

“We had expected that rising costs would weaken profitability in 2019,” said de Juniac. “However, the sharp fall in oil prices and solid GDP growth projections have provided a buffer.”

Cargo Facts Free Newsletters