Will growth in the US Domestic Air Express market continue?

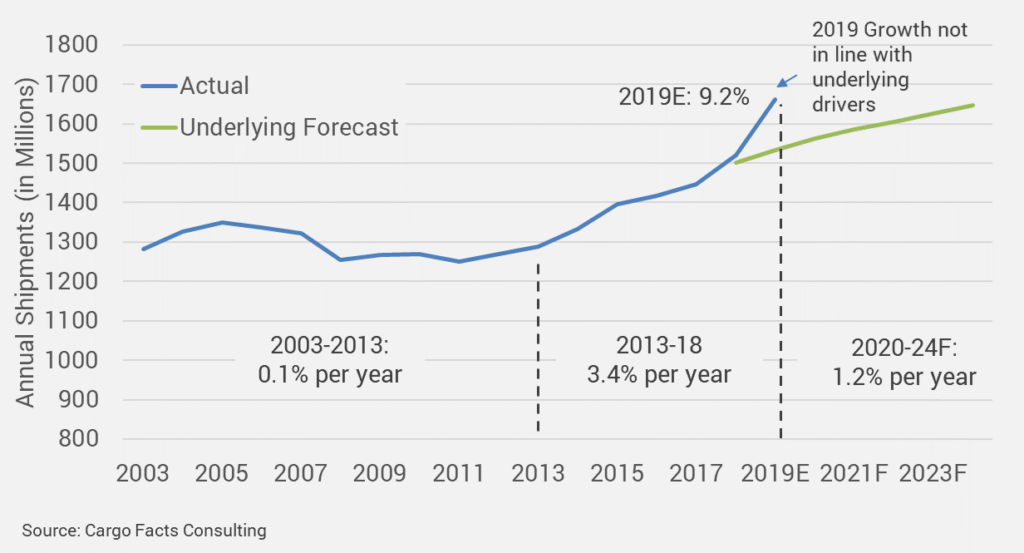

Average shipment growth in the past five years accelerated to 3.4% and in 2019 we expect a whopping 9.2%. This compares to average growth of 0.1% per year in the 10 years prior, during which the market experienced poor economic conditions, a decline of document traffic, and the withdrawal of DHL Express following its failed acquisition of Airborne Express.

Much of the growth of late has been driven by a surge in e-commerce traffic, which according to our research accounts for almost half of worldwide express shipment volumes. However, as e-commerce platforms such as Amazon move to in-source volumes, we believe that much of this recent growth may be lost. Consequently, we are forecasting underlying growth of only about 1.2% per year for the next two years, based on figures preceding the pre-2019 surge (see Figure 1).

Figure 1 – US Domestic Express Shipments 2003 – 2024F

Would this be a bad outcome for the U.S. domestic express business? The loss of this business may be good for yields, but both FedEx and UPS have been making large investments in anticipation of continued volume growth.

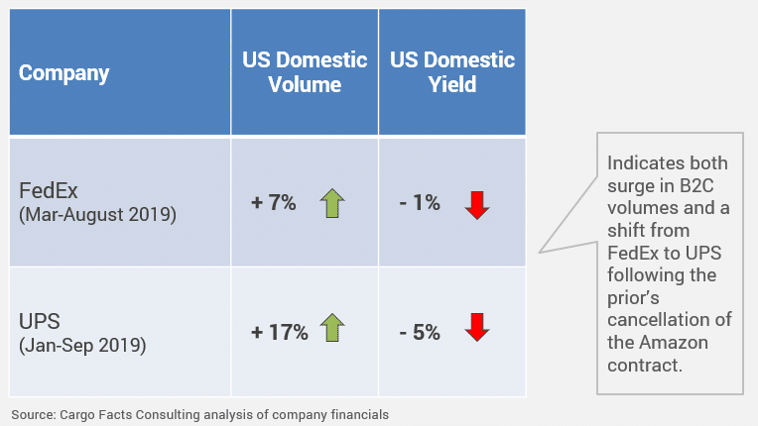

Volume growth, particularly in 2019, has come at the expense of lower yields. For example, UPS reported a 17% increase of US domestic (next day and deferred) package volumes, but a 5% drop in yields. A sizeable portion of the increase is due to a shift in Amazon volumes following termination of the FedEx contract in June. Predictably, FedEx shipment volume growth has been more moderate, and the company has fared better from a yield perspective, registering only a 1% decline in yields during the six months ended August (see Figure 2).

Figure 2 – FedEx and UPS Package Volumes and Yields in 2019

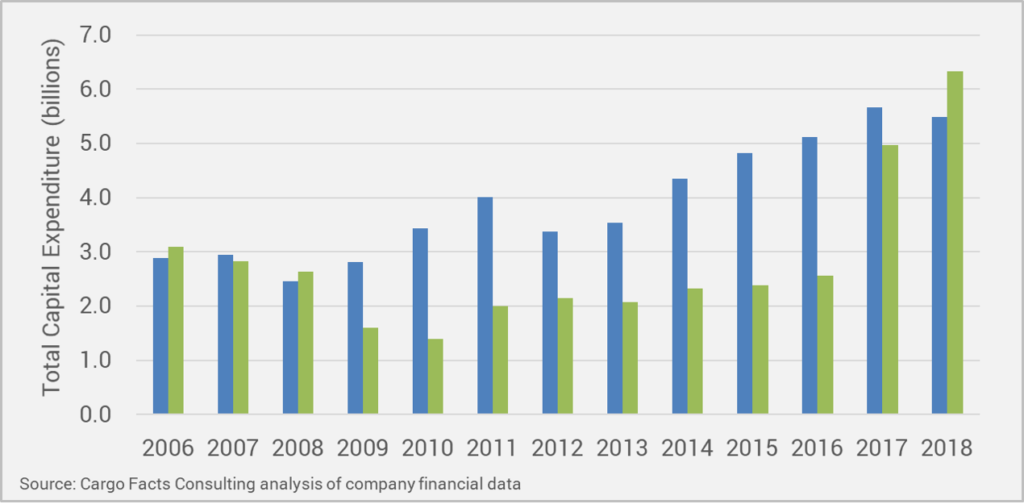

The most immediate response of the Express business to the changing market and competitive environment has been to invest heavily in capacity and service improvements, while also implementing measures to reduce last-mile delivery costs. Both FedEx and UPS have increased investment over the past several years to cater for additional growth (see Figure 3).

Figure 3 – FedEx and UPS CapEx 2006 – 2018

UPS, in particular, has increased its share of capex as a percentage of revenue from 5% in 2016 to 9% in 2018. UPS capital expenditure is expected to increase a further 10% in 2019. Most FedEx and UPS investments are in infrastructure improvements, sorting facilities and technology. The key question will be whether all this additional capacity finds use or whether there may be overcapacity in the market going forward. In the last five years, the U.S. domestic express market has gone from a mature to a growth market again, but how long can that dynamic last?

Next week, Cargo Facts Consulting will publish a new report, the Air Express Market Outlook 2020 – 2024, which looks at how e-commerce and emerging competition are disrupting the business. This is the first of a series of articles that showcase some of the findings of the report.

Frederic Horst is Managing Director of Cargo Facts Consulting. He can be reached via www.cargofactsconsulting.com.

{kind=link}

Cargo Facts Free Newsletters